Outlook for the global economy and financial markets

Resilience despite uncertainties

The market environment at the beginning of 2026 is characterised by remarkably high economic resilience – despite geopolitical tensions, political uncertainties, inflation risks, and increased volatility. The growth forces at play have remained astonishingly robust and key technology trends – above all the AI boom – continue to provide support.

At the same time, the list of risk factors remains extensive: geopolitical conflicts, cooling employment dynamics in the USA, high government debt in numerous countries, and political missteps could lead to setbacks at any time.

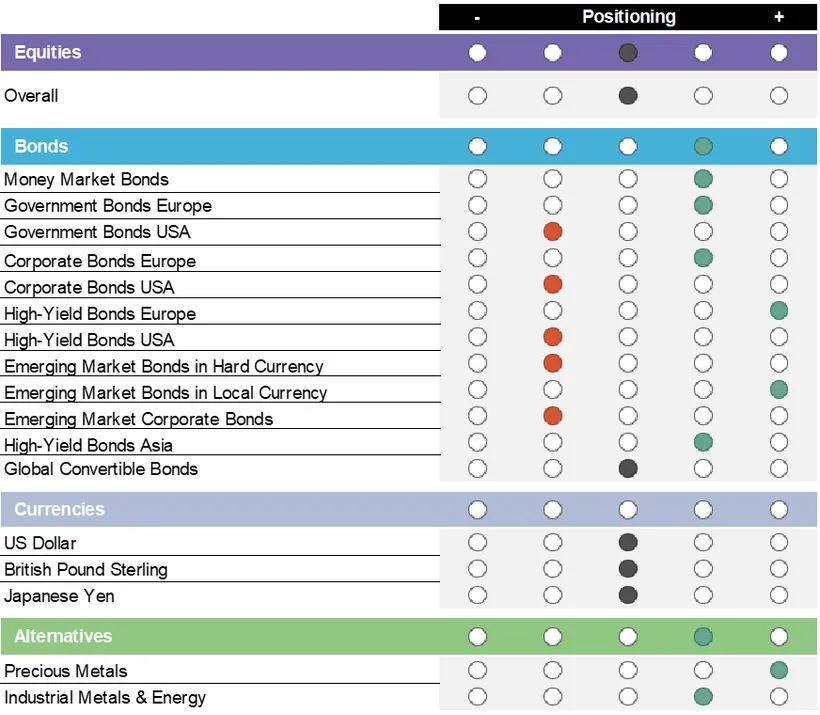

Equities – balanced, with clear preference for value

Despite the favourable market environment, our equity allocation remains neutral. The valuation levels of many leading indices are close to historic highs, which limits short-term upside potential. It is therefore crucial to take a differentiated view of fundamentals and trends: as long as corporate earnings continue to grow, there is every reason to believe that the market will remain robust.

Regionally, we are focusing more strongly on Europe because of more attractive valuations. We are deliberately underweighting the United States, as high valuations, an uncertain political agenda, and fiscal risks are clouding the outlook. Japan, on the other hand, remains neutrally positioned.

In addition, we are increasing our exposure to India, which continues to show economic growth and favourable momentum. In Latin America, we are taking advantage of the combination of low valuations, commodity-heavy markets, and an increasingly stable monetary policy situation, and we are optimistic.

We are also pursuing a consistent approach with regard to sectors and factor strategies: we favour value shares, particularly in the USA and Europe. In addition, we are betting on European small caps, which are benefiting from economic tailwinds, as well as high-dividend quality companies that combine earnings and stability.

We remain committed to the healthcare sector due to its defensive characteristics, while the energy sector in Europe is benefiting from transformation and supply factors.

Please note: investing in securities involves risks as well as opportunities.

Bonds – neutral duration, but clear preferences among regions

In the bond segment, we are maintaining a neutral duration, albeit with significant nuances in regional allocation. We prefer bonds from the Eurozone, where declining inflation and more stable political conditions are supporting the environment.

On the emerging markets front, we pursue a two-pronged approach:

- Local currency bonds benefit from stable currencies and continued interest rate cuts by many emerging markets central banks – please see the article “Bonds in a world of inflation risks and yield expectations”.

- Hard currency bonds, on the other hand, remain underweighted as they are more dependent on the US interest rate environment and possible fluctuations in US Treasuries.

Within the Eurozone, we also see clear differences among countries: although the change in fiscal policy in Germany offers hope for European convergence, it also brings uncertainties, which is why we take a rather defensive stance vis-à-vis Germany. We see opportunities on the Iberian Peninsula and in Italy, which are benefiting from higher interest rates and carry effects.

Commodities – gold as stability anchor, industrial metals with structural tailwind

Gold remains a key component of our portfolio. It serves not only as a hedge against geopolitical shocks and structural inflation risks, but increasingly also as a safeguard against potential losses of confidence in political institutions and currencies – particularly the US dollar.

Despite short-term headwinds such as weak global manufacturing and the struggling Chinese construction industry, we continue to see a structurally positive outlook for industrial metals. Technological change – driven by artificial intelligence, electromobility, and the energy transition – is creating additional demand, while low inventories are limiting supply.

Energy, on the other hand, remains underweighted: global supply exceeds demand. Only geopolitical outliers, such as possible escalations in Iran, could trigger temporary counter-movements.

Currencies – balanced, while keeping an eye on political risks

The prevailing view on the US dollar is neutral. Although the technological strength of the US economy provides structural support for the dollar, unconventional political decisions and the chronically high budget deficit are weighing on its attractiveness. Despite its favourable real valuation, the Japanese yen also remains neutral, as the Bank of Japan's expected interest rate moves are already largely priced in.

Conclusion of our investment strategy

Broad diversification, focus on quality, balanced risk positioning, and selective opportunities in value shares, emerging markets local currency bonds, and commodities – especially gold.

Source: Erste Asset Management, January 2026

Notes: Forecasts are not a reliable indicator of future performance. Where fund portfolio positions are disclosed in this document, they are based on market developments as at 29/01/2026. These portfolio positions may change at any time as part of active management. Please note that investing in securities involves risks as well as the opportunities described.

For explanations of technical terms, please visit our Fund Glossary.

Disclaimer

This document is an advertisement. Please refer to the prospectus of the UCITS or to the Information for Investors pursuant to Art 21 AIFMG of the alternative investment fund and the Key Information Document before making any final investment decisions. Unless indicated otherwise, source: Erste Asset Management GmbH. Our languages of communication are German and English.

The prospectus for UCITS (including any amendments) is published in accordance with the provisions of the InvFG 2011 in the currently amended version. Information for Investors pursuant to Art 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in connection with the InvFG 2011. The fund prospectus, Information for Investors pursuant to Art 21 AIFMG, and the Key Information Document can be viewed in their latest versions at the web site www.erste-am.com within the section mandatory publications or obtained in their latest versions free of charge from the domicile of the management company and the domicile of the custodian bank. The exact date of the most recent publication of the fund prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the Key Information Document are available, and any additional locations where the documents can be obtained can be viewed on the web site www.erste-am.com. A summary of investor rights is available in German and English on the website www.erste-am.com/investor-rights as well as at the domicile of the management company.

The management company can decide to revoke the arrangements it has made for the distribution of unit certificates abroad, taking into account the regulatory requirements.

Detailed information on the risks potentially associated with the investment can be found in the fund prospectus or Information for investors pursuant to Art 21 AIFMG of the respective fund. If the fund currency is a currency other than the investor's home currency, changes in the corresponding exchange rate may have a positive or negative impact on the value of his investment and the amount of the costs incurred in the fund - converted into his home currency.

Our analyses and conclusions are general in nature and do not take into account the individual needs of our investors in terms of earnings, taxation, and risk appetite. Past performance is not a reliable indicator of the future performance of a fund.