Outlook for the global economy and financial markets

Geopolitical détente meets robust growth

The global economic environment remains fundamentally robust as we reach mid-2026. Growth continues to hover close to potential and is underpinned by stable consumer demand, rising investment, and structural impetus from the AI boom.

A significant change has resulted from the recent easing of tensions in the Iran conflict: the agreement between the United States and Iran and the prospect of the Strait of Hormuz reopening considerably reduce the risk of a prolonged energy price shock. The geopolitical risk premium previously priced into the market has already fallen significantly, as reflected in falling oil prices and a positive market reaction.

This confirms our base-case scenario of “inflationary growth” – now with more moderate tail risks and a more stable environment for financial markets.

Inflation and monetary policy – pressure is falling, but remains high

Inflation will remain above target in the short term, driven by previous rises in energy prices and structural factors such as the AI-driven investment cycle.

As conditions on the energy markets ease, inflationary pressures are gradually subsiding. This reduces the risk of a sustained inflationary shock and gives central banks more room for manoeuvre. We continue to expect a slightly restrictive monetary policy, but without aggressive interest rate hikes.

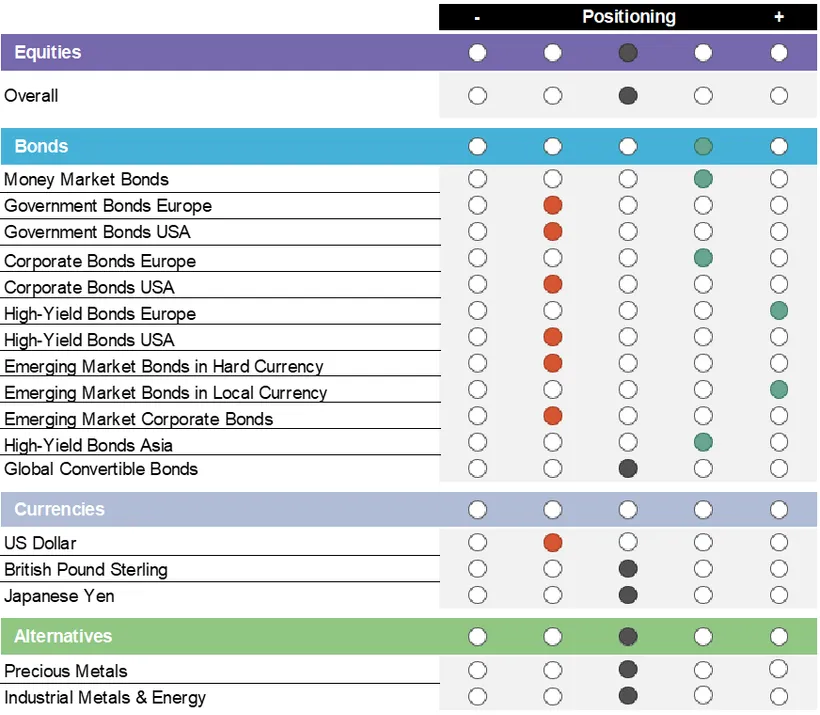

Equities – neutral with selective opportunities

The easing of tensions in the Middle East is clearly providing a boost to risk assets. The reduction in geopolitical tail risks, falling energy prices and more stable inflation expectations are improving the fundamental environment for equities. However, please also bear in mind the risks associated with investing in securities.

We are raising our equity allocation from underweight to neutral as:

- Valuations remain ambitious

- Earnings expectations remain high

- Part of the positive trend is already priced in

Our strategic preferences are being confirmed across the equity markets:

- Focus on structural winners (particularly US technology / AI)

- Value and dividend strategies as anchors of stability

- Europe and small caps with catch-up potential

- Latin America and Japan as attractive value markets

Further tailwinds are now emerging from falling input costs (energy), which should support margin growth in cyclical sectors.

Bonds – carry remains attractive, duration slightly short

In the bond segment, the easing of pressure on the energy market reduces the risk of a sudden rise in yields. Nevertheless, we remain cautiously positioned:

- Duration: slightly underweight – as inflation remains above target

- Government bonds: underweight – limited yield potential despite the easing of tensions

- EUR corporate bonds: overweight – attractive spreads

- EM local-currency bonds: overweight – also benefitting from more stable global conditions

Overall, we favour a shorter duration positioning. On the yield curve, we currently prefer moderate positions that benefit from a widening yield spread. On the whole, the environment for carry strategies remains supportive – albeit amid lower volatility.

Commodities – drastic decrease in energy price risk

The commodity markets are reacting particularly strongly to the easing of geopolitical tensions. Previously, the closure of the Strait of Hormuz and the attacks on energy infrastructure in the region had led to a sharp rise in oil and gas prices.

- Energy: neutral (with a downside bias) – the reopening of the Strait of Hormuz is leading to an increase in supply and a significant decline in risk premiums. In the short term, however, technical factors (transport, resumption of production) remain relevant.

- Industrial metals: neutral – the AI boom and rising industrial demand remain key drivers.

- Gold: neutral – slight headwinds due to receding geopolitical risks, but still supported by structural factors (debt, long-term inflation).

Currencies – a more stable environment, but structural factors are the dominant factor

- USD vs. EUR: neutral

- Positive: strong US growth driven by the AI boom

- Negative: rising US budget deficit and claims for tariff refunds

- GBP vs. EUR: neutral

- A slowdown in the labour market and a stagnant economy

- JPY and EUR: neutral

- The Bank of Japan’s interest rate hike versus negative real interest rates

Conclusion of our investment strategy

- Broad diversification

- Focus on quality

- Balanced risk positioning

- Selective opportunities in equities (value and dividend) and bonds (carry, especially EUR credit and EM local currencies)

Source: Erste Asset Management, June 2026

Notes: Forecasts are not a reliable indicator of future performance. Where fund portfolio positions are disclosed in this document, they are based on market developments as at 10/06/2026. These portfolio positions may change at any time as part of active management. Please note that investing in securities involves risks as well as the opportunities described.

For explanations of technical terms, please visit our Fund Glossary.

Disclaimer

This document is an advertisement. Please refer to the prospectus of the UCITS or to the Information for Investors pursuant to Art 21 AIFMG of the alternative investment fund and the Key Information Document before making any final investment decisions. Unless indicated otherwise, source: Erste Asset Management GmbH. Our languages of communication are German and English.

The prospectus for UCITS (including any amendments) is published in accordance with the provisions of the InvFG 2011 in the currently amended version. Information for Investors pursuant to Art 21 AIFMG is prepared for the alternative investment funds (AIF) administered by Erste Asset Management GmbH pursuant to the provisions of the AIFMG in connection with the InvFG 2011. The fund prospectus, Information for Investors pursuant to Art 21 AIFMG, and the Key Information Document can be viewed in their latest versions at the web site www.erste-am.com within the section mandatory publications or obtained in their latest versions free of charge from the domicile of the management company and the domicile of the custodian bank. The exact date of the most recent publication of the fund prospectus, the languages in which the fund prospectus or the Information for Investors pursuant to Art 21 AIFMG and the Key Information Document are available, and any additional locations where the documents can be obtained can be viewed on the web site www.erste-am.com. A summary of investor rights is available in German and English on the website www.erste-am.com/investor-rights as well as at the domicile of the management company.

The management company can decide to revoke the arrangements it has made for the distribution of unit certificates abroad, taking into account the regulatory requirements.

Detailed information on the risks potentially associated with the investment can be found in the fund prospectus or Information for investors pursuant to Art 21 AIFMG of the respective fund. If the fund currency is a currency other than the investor's home currency, changes in the corresponding exchange rate may have a positive or negative impact on the value of his investment and the amount of the costs incurred in the fund - converted into his home currency.

Our analyses and conclusions are general in nature and do not take into account the individual needs of our investors in terms of earnings, taxation, and risk appetite. Past performance is not a reliable indicator of the future performance of a fund.